Give a Gift

NextGen 529 contributions make fantastic holiday, birthday, or “just because” gifts. Grandparents, other family, or friends can all give to your account.

Even better? If either the account owner or beneficiary is a Maine resident, gifts can be matched by 30%, up to a $300 grant per year, with Maine’s annual NextStep Matching Grant.1

PROVIDE FOR THE FUTURE

How to Make a Gift

To make a gift contribution to a NextGen 529 account, the gift giver2 should:

Write a Check

Be sure your check is made payable to: “NextGen 529 FBO [Beneficiary/Student Name]”

Fill Out Contribution Coupon

Complete a contribution coupon, being sure to include the account number of the beneficiary/student.

Pop in the Mail

Mail to: Merrill Edge

P.O. Box 962

Newark, NJ 07101-0962

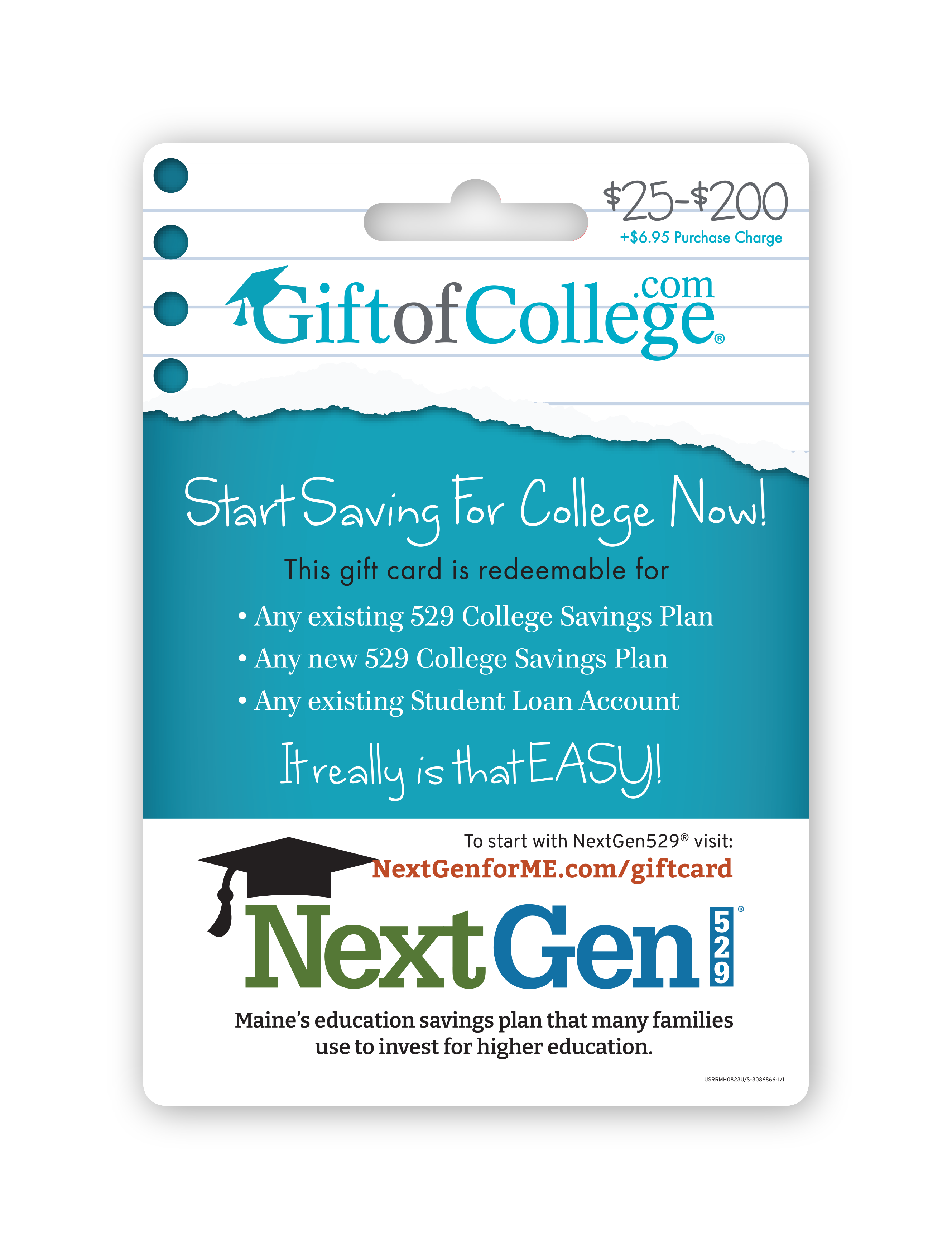

Gift Cards for College

Buy a Gift of College gift card to give the gift of higher education to the special student in your life. NextGen 529-branded Gift of College gift cards are available at CVS stores in Maine or online.

Did you receive a Gift of College Gift card?

Learn more about adding the gift card to your NextGen 529 account and answers to frequently asked questions.

Make It Extra Special

Whether grandparents are looking for a gift for a child who has outgrown toys, family members want to recognize the first day of kindergarten, or friends want to give a very special birthday gift, using one of our occasion cards completes the gift. Make planning and saving for college even more fun with a special card or by using the time capsule kit.

Download and Print a Custom Card

There are cards for many special occasions–from birthdays and holidays to “just because.” Simply add your name and the child’s name, roll it up and tie it with a bow.

Check Out our Time Capsule Kits

The Time Capsule Kit is a gift that will last a lifetime and gets your child thinking about their future self.

See a 529 Savings Picture

When you save with a 529 plan, you’re not just setting money aside – you may decrease the amount you may need to borrow and repay with interest later. This calculator helps you explore how investing in a tax-advantaged 529 plan compares to a non-tax advantaged account. Plus, see the difference between saving in 529 plan now in comparison to borrowing and repaying with interest later.

ESTATE PLANNING

Planning Ahead

Contributing to a NextGen 529 account can be an attractive option for anyone wishing to help fund college for a special student in their life—and provides estate-planning benefits.

A contribution to a 529 plan account is treated as a completed gift from the giver to the recipient (the designated beneficiary of the 529 account) and qualifies for the annual federal gift tax exclusion of $19,000 ($38,000 for married couples filing jointly), per beneficiary.

You may also be able to take advantage of a federal gift tax election that applies only to 529 plan contributions. This election allows a lump-sum contribution of up to $95,000 ($190,000 for married couples filing jointly), which is five times the annual exclusion amount, per beneficiary in one year, and treats the contribution as if it was made ratably over five years.3 Please consult your tax and/or legal advisor for specific guidance before making investment decisions that could affect your taxes or estate or Medicaid planning needs.

1Grants for Maine Residents are linked to eligible Maine accounts. An Alfond Grant recipient is eligible to receive the $100 Initial Matching Grant if the minimum required initial contribution is made before the beneficiary’s first birthday. Upon withdrawal, grants are paid only to institutions of higher education. See Terms and Conditions of Maine Grant Programs for other conditions and restrictions that apply. Grants may lose value.

2Third-party contributions: Persons other than the account owner who make contributions will have no subsequent control over the funds contributed to a NextGen 529 account. Only the NextGen 529 account owner will receive confirmation of account transactions and may direct transfers, rollovers, investment changes, withdrawals and change the account beneficiary (as permitted under federal law). Third-party contributors may subject NextGen 529 account owners to tax consequences. NextGen 529 account owners and third-party contributors should consult their tax advisors to discuss income or gift tax consequences.

3If you make the five-year election to prorate a lump-sum contribution that exceeds the annual federal gift tax exclusion amount and you die before the end of the five-year period, the amounts allocated to the years after your death will be included in your gross estate for tax purposes. Please note that when making a contribution to a 529 account (whether for a single year or using the special election to prorate the gift over five years), all other gifts you make to a particular beneficiary are included in determining the available annual gift exclusion amount.